Having kids transforms the way you think about the future. You’re no longer living only for yourself, or only for yourself and your partner. A child creates its own set of obligations and responsibilities, and nowhere is that more true than when it comes to finances. Below are 10 steps my husband and I took to financially prepare for having our son.

1. Planned our parental leave

Around the time I was 16 weeks, I set up a meeting with my HR to discuss the conditions of my leave. As luck would have it, my employer revamped its benefits in January and I learned I’d be allowed a total of 26 weeks off! The first 8 weeks would be covered through short-term disability, the next 12 weeks under my employer’s maternity leave benefits, and the last 6 would be unpaid time off. Not surprisingly Tommy got significantly less time off than I did, but my contention with US companies having lackluster parental leave programs (especially for dads) will be reserved for another day.

2. Updated our budget

After my discussion with HR I updated my budget to account for my short-term disability (where I’d only be receiving 67% of my pay) and 6 weeks of unpaid leave. Something I learned while receiving STD pay is that while it was only 67% of my salary, there were no deductions or income taxes taken out. This resulted in me basically receiving my standard paychecks, if not a little more. The other nuance with STD is that you receive it in 2 lump sum payments. Because of this, I modified my contributions to savings and investments to happen at the beginning of the month instead of on the days I would normally get paid.

3. Opened a 529 account for baby

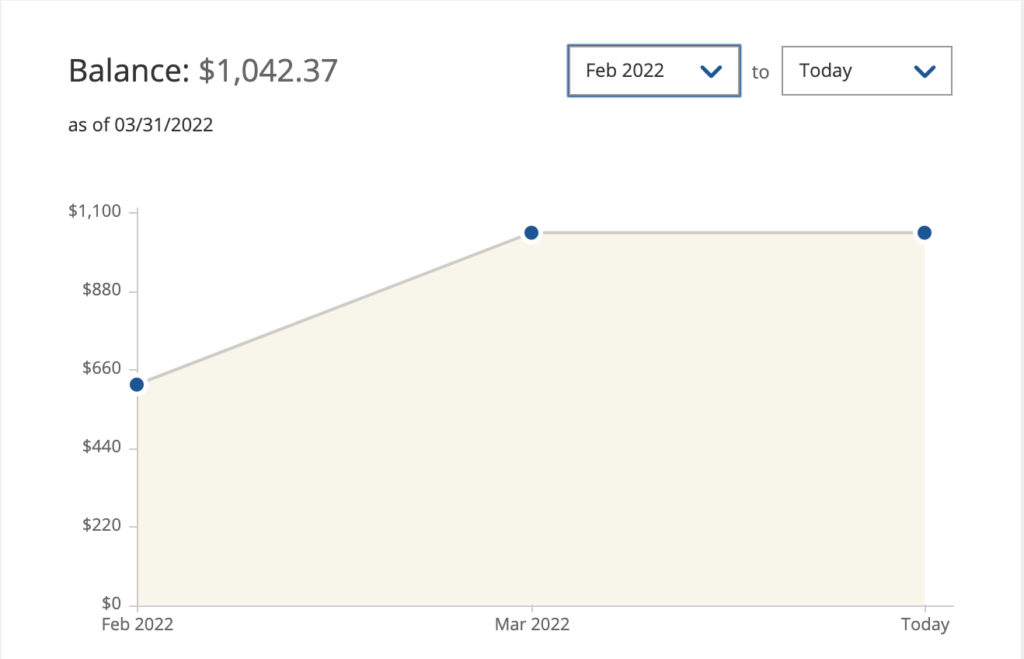

I’ve discussed in previous posts how I’m a fan of 529 accounts to save for your children’s education. I actually opened up our son’s college account a month before he was born and made the first contribution using money we were gifted as baby shower and Chinese New Year gifts. In total we’ve contributed a little over $900 and the account is already at over $1,000 from investment gains.

If you’re wondering how I opened the account before he was born, I put it in my name and listed myself as the beneficiary. 529 accounts will let you change beneficiaries penalty-free at least once a year. So now that Luca is earth side with us I’m able to update him to be the beneficiary.

Tommy and I will start by funding this account with $200-300 a month and also put baby’s future monetary gifts here. This may change over the years if I feel we’re underfunding/overfunding or if Luca shows signs of being a baby Einstein and attends university on scholarship (please ancestors, let it be the latter!). But Amy, what if he wants to become an electrician or mechanic? 529 accounts can be used toward trade schools and certificate programs as well so we’ve got him covered. But we’ve also already decided he’ll be a doctor or NBA player because we’re Asian tiger parents so the last point I just made doesn’t actually apply to him.

A couple of things I want to call out:

- Saving for your child’s future education is a personal choice. I know people who don’t believe in doing this and others who wish they could but don’t have the means. I, myself, was not fortunate enough to receive aid from my parents for college and I did just fine. This brings me to my second point.

- I’m not opposed to my kid(s) taking out school loans if they need to. I have no idea how much college will cost in 18 years. Whatever shortfall this account ends up having, I’m confident my child will have the resources to asses his options.

- I would not recommend saving for your child’s future college education at the expense of your own retirement! I’ve heard of people taking out second mortgages or reducing their 401(k) contributions so they can contribute to their child’s college accounts. This is wild to me. Your children can take out loans to fund school. You cannot take out loans to fund your retirement.

- I opened my son’s account before he was born in order to get an early start on his contributions. However, I wouldn’t recommend doing this too early in the unimaginable case you aren’t able to carry out your pregnancy. I waited until I was about 8 months pregnant, but ultimately do what you’re comfortable with.

4. Planned ahead for medical expenses

News flash: Having a baby is expensive. It’s the most costly health event families are likely to experience during their childbearing years. One study found the average cost of giving birth was $4,500—even with insurance. That’s including pregnancy, labor and delivery, and three months of postpartum care.

Currently, I have a $3,000 deductible with my HDHP insurance plan. Prior to giving birth, I hadn’t met much of this since the new year had just started. I knew I’d satisfy the deductible with my hospital stay so I earmarked this amount in our savings ahead of time. I do have an HSA that currently has around $8k in it, but I’m reserving those funds for retirement so I planned early on to pay the deductible out of pocket. The nice part about reaching my deductible in February is that my medical expenses will be covered at 100% for the remainder of the year.

5. Called my insurance provider

My employer switched insurance carriers in January so I called them in advance to make sure my OBGYN, delivery hospital, and pediatrician were all in network with the new plan. This should be standard practice, but I’m always surprised at how many friends and family members don’t call and check ahead of time and then get stuck with out-of-network statements. This simple step can save you thousands of dollars!

6. Took inventory of our baby items

After our baby shower I took inventory of how many diapers, wipes, and sleepers we received for every size up to 12 months. Surprisingly we had way too many of some sizes and barely enough of others. This was helpful in making sure we returned the excess stuff we didn’t need and exchanged them for sizes we were missing or gift cards for later use.

7. Stayed on course with savings & retirement

Both Tommy and I continued funding our emergency fund, HSA, IRA, and 401(k)s per usual. Even with my unpaid leave, I made sure my spending was adjusted during that period to not affect my savings and investment goals.

8. Reevaluated living needs

Once we found out I was pregnant, we decided to reevaluate our vehicle and living situation. Tommy had been wanting to upgrade his car to an SUV for awhile to combat the harsh Minnesota winters. With baby on the way it made sense to pull the trigger to accommodate our growing family. We ended up selling his old car and ordered our Kia Telluride in October. It just arrived a couple weeks ago and is already serving our family wonderfully!

Another topic that has been on our mind for quite some time now is moving. We’ve been in our current home for 5 years now and for the last year or so have felt like we’ve outgrown the size and layout. With baby here, we’re extra motivated to move but with the market being as crazy as it is – we haven’t found anything we love. We’ve continued our search and are hoping within the next 1-2 years we can find something.

9. Treated ourselves 😀

Being financial responsible to us doesn’t just mean saving. It also means spending our money on things that bring us joy. It was important for the both of us to celebrate the news of our growing family and also spend time connecting with one another before baby arrived. We decided to do both by treating ourselves to a babymoon. We spent a week in Oceanside, CA (a beach town about an hour north of San Diego) soaking up the sun, relaxing poolside, walking the night markets, and eating delicious meals. It was one of my favorite trips we’ve taken together.

10. Purchasing life insurance & establish a will

Okay, technically this one is a pending item but having a tiny human rely on you for financial support means you have to ask yourself the hard question of “What happens to my child or partner if I die?”. Acquiring life insurance is one way to provide for your family financially if you die before you expect to. Tommy and I plan to purchase a term plan with the expectation that in 20 years our son will be financially independent, our mortgage will be mostly paid off, and we’ll have accumulated enough savings for the other to live comfortably in retirement. Additionally, we plan to update our will to designate a guardian for our son.

[…] has been Tommy’s dream car since the flagship model came out in 2019. I mentioned in my previous post that we ordered ours at the end of 2021 and it finally arrived in April 2022. We put ~$34k down to […]