In February I wrote a post about the financial goals I was setting for me (and Tommy) this year. Though a lot of things went our way this year, a few things didn’t. In today’s post I’m sharing our financial successes and misses from 2021.

Successes:

● Paid off all debt (outside mortgage)

Okay I know I talked about this in my last post but seriously, I will never stop bragging about the fact that I paid off my grad school loans (~$40k) and car note (~$10k) all by myself last year. I DID THAT.

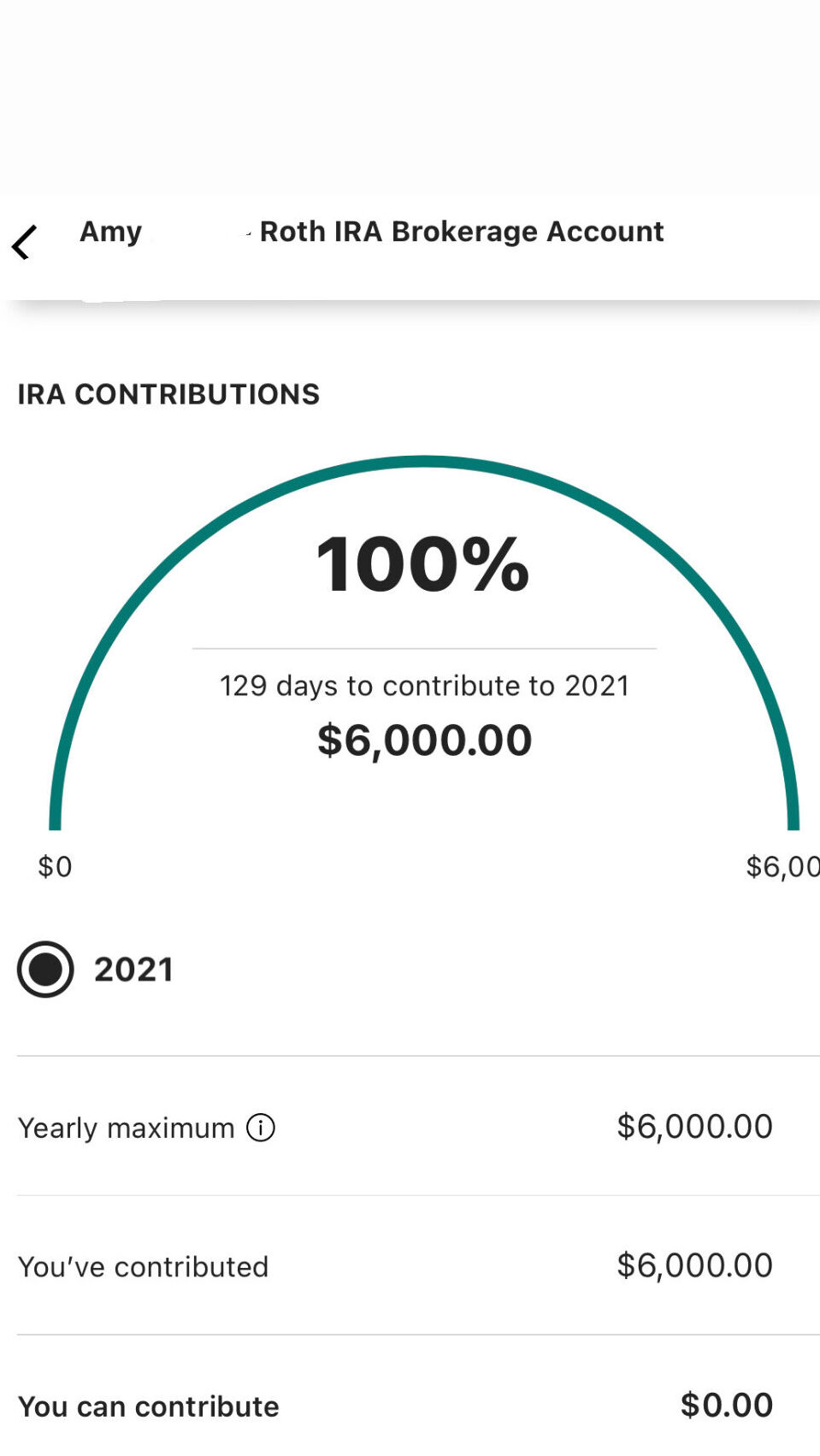

● Maxed out my 2021 Roth IRA Contribution ($6,000)

I automatically transfer $250 per paycheck into my Roth IRA at Vanguard. Because my employer switched from a bi-monthly pay schedule to a bi-weekly, my contributions max out every November. I like using the Dollar Cost Average method when it comes to investments as this strategy has always worked well for me.

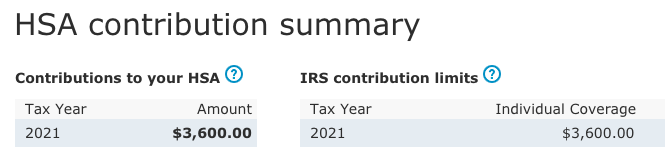

● Maxed out my 2021 HSA Contribution ($3,600)

This is another automated savings I have set up, except this one is through my employer’s payroll. I maxed out my HSA contributions by October of this year so it was nice to have a little more take home money the last 3 months of the year (’cause holidays & big Asian families = expensive yuletides).

The IRS announced the annual limit would increase by $50 for individual plans next year, bringing it to $3,650. As an added bonus, my employer will start contributing $500 to my HSA next year which counts toward the annual limit. This means I’ll only need to funnel $3,150 through my standard payroll next year!

● Increased my 401(k) contributions

As shared above, by March of this year I had paid off my school loans, car note, and was also able to drop Tommy from my medical insurance because he finally became eligible under his employer’s plan. With the huge lift of these monthly expenses I was able to increase my 401(k) contributions by 3%, bringing my annual contribution to 11%.

● Got a promotion and, more importantly, a raise!

This really was my biggest financial ‘win’ of the year. In September I was promoted to Senior Manager at my company after only 11 months! The promotion came with a generous 17% raise. I’m now making 48% more than I was just one year ago! The increase in cash flow helped fund a lot of our goals and expenses this year.

The most rewarding part of this experience was that I wasn’t up for a promotion – I actually asked for one. I plan to write a separate post dedicated to this topic as it involved me taking a leap of faith which ended in my favor! The entire experience taught me a lot about assessing my value in the work place and I’m excited to share more about what I learned.

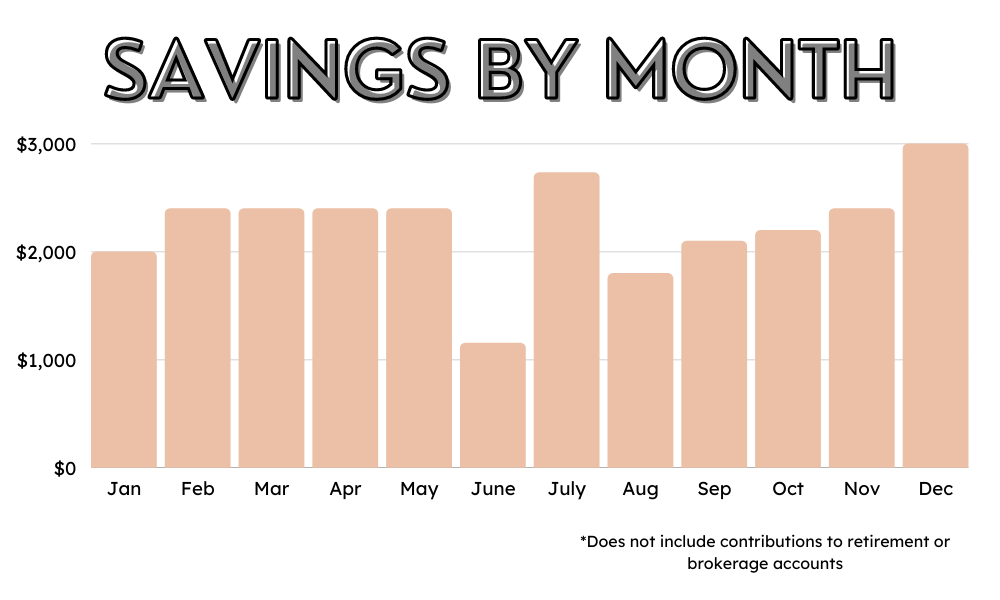

● Saved ~$27,000

Tommy and I automate our savings every month into our online HYSA. This year we saved a combined total of $26,989. Our original goal was to save $28,800 which means we fell short by $1,811. Not bad considering how many large expenses came up this year. More on that below!

Misses:

You’ll notice I didn’t use the word “failures” cause I don’t like to think of financial misses as failures. Life is unpredictable and unplanned events and expenses happen. The best you can do is assess, adjust, and stay consistent.

● Limit monthly spending to $1200

If you recall from my February post, I increased my monthly spending budget from $800 to $1,200. Turns out I grossly underestimated what my actual spending would be 😅 My average monthly spending in 2021 was closer to $1,600. However, I’m not beating myself up over this miss! I consider myself a mindful spender and know that my lifestyle has changed quite a bit from even a year ago. I accept that my personal and professional growth have afforded me a very comfortable lifestyle and there is no 👏 shame👏 in👏 that👏 honey.

● Make $200/month in side hustles

This was one of the goals I set for myself this year. I hit this goal 5 out of the 12 months. I did this primarily buying and reselling home decor items I thrifted or purchased off of FB Marketplace. To be honest, I just wasn’t motivated after the first few months of the year to do a ton of things on the side. As the year progressed so did my projects at work. As a result, I put little to no emphasis on reaching this goal. I don’t know that I’ll be a huge “side hustle” person going forward and that’s okay with me.

● Large expenses

We had a number of large unexpected expenses this year that required us to dig into our savings:

- In January I took $3,600 out of our savings to pay off the remainder of my grad school loans

- In March we remodeled our bathroom. And while we were able to fund the majority of the project through our normal cash flow, we did end up taking out about $2k from our savings to pay for part of it

- In May we took out $1,000 to pay our tax bill

- In July, Tommy took out $5k to invest in his company’s stock options

Total withdrawals = $11,600

2022 Plans…

If you follow me on my other social media platforms you know my husband and I are expecting our first child together! Baby Luca is expected to arrive early next year and has been a huge motivation in us amping up our savings and also making changes to our financial planning for next year. Much of our goals will stay the same but a few additions include:

- Open a 529 account for Baby Ng

We plan to open a college account for baby as soon as he’s born. We know that college is not for everyone, but we’re both strong advocates for postsecondary education and the lifelong benefits and doors of opportunity that it enables. We’ll start by putting $200/month into the account to begin with and funnel any monetary gifts baby gets into this account to save for future college expenses. - Buy a new car

A year of no car notes was nice but 2022 is looking to change that with the arrival of Baby Luca! Tommy decided it would be best to upgrade his car to an SUV for safer family travel. We actually ordered our new 2022 Kia Telluride last month but it won’t arrive until February or March. We’ll be trading in Tommy’s car and putting a sizable cash down payment on the vehicle to keep our borrowing amount minimal. - Increase monthly spending budget to $1,500

With Baby Luca’s arrival early next year I don’t expect we’ll be doing a ton of travel or entertaining. Still, I plan to err on the conservative side and increase my monthly spending next year.

Leave a Reply