Hi, remember me? It’s been a minute since my last post. Most of my writing breaks in the past have been due to pure laziness but this one was warranted. Not long after the re-launch of my blog in May, the murder of George Floyd happened here in my beloved city of Minneapolis. The civil uprising that occurred as a result of that event, coupled with the global pandemic took a toll on my spirit and mental health. For a long time posting on my blog or social media felt like unnecessary noise. It’s taken several months but slowly, I’m finding the capacity to be creative and find joy in this space again. And while I haven’t been vocal about my financial journey in awhile, that doesn’t mean I haven’t been putting in the #WERK. A lot has happened this year and I’m excited to share them with you all – especially those of you who have been invested in my financial journey since my blog’s inception.

2020 Updates

I finished school!

That’s right, I’m a Master now and will only accept being referred to as such. In typical fashion of Asian parents, my mom voiced how proud she was of me by asking why I was settling for anything less than a PhD 😒

I got a new job!

I started at my new company at the end of October. My first day was actually on my birthday so the entire day felt like a big birthday present from the universe! Switching companies after being with my previous firm for only 13 months came as an unexpected surprise, even to me. But I was offered an amazing opportunity at a FinTech company whose product promotes financial wellness and I just couldn’t pass it up! I’m officially a month into the role and have had more fun than I’ve had in my last 5 years of working in Finance. Am I possibly still wearing rose-colored glasses and sipping the Silicon Valley Kool-Aid? Probably, but it’s 2020 so I’ll take all the feel-goodz I can get.

New job = more money!

Along with all the opportunity my new company has already offered me – it also came with a 27% increase in my base salary alone. This doesn’t include equity + bonuses that are part of my compensation package as well. I’m finally at a salary level I feel satisfied with and you bet I put together a plan on how I’d be allocating that raise right away.

My husband lost his job

It wouldn’t be a 2020 update if we didn’t sprinkle some bad news in here too, amirite? In March, Tommy landed his dream job at a tech firm only to be laid off due to the economy a month later. It seemed surreal to have everything he could ever hope for in a role and company be taken away from him as soon as he got it. And like millions of others who experienced similar situations – we were both devastated. We knew there’d be financial repercussions in our household so we took measures to prepare ourselves for the uncertainty of his future return to work:

- Tommy picked up shifts 3 days a week at his family’s restaurant. Thankfully, the local community has rallied around supporting them during the pandemic and his parents were happy to take the additional days off for him to fill in.

- Tommy secured an IT consulting gig which pays him a monthly fee regardless of whether they utilize his help or not. So far it’s only required about 5-10 hours of his time a month so it’s been a great gig and has helped in recovering his lost income.

- We both stopped contributing to our Roth IRAs for several months to beef up our savings.

- We worked toward increasing our emergency fund from 6 months worth of expenses to 12 months and saved as much as we could, whenever we could.

- I was super active in selling a lot of our unused home items on FB Marketplace over the summer. Tommy actually took up wood working and sold a bunch of his builds through Marketplace as well. This helped our cash flow a lot and allowed us to continue being aggressive in our savings + debt paydown goals. Speaking of debt & savings – let’s update you on that too.

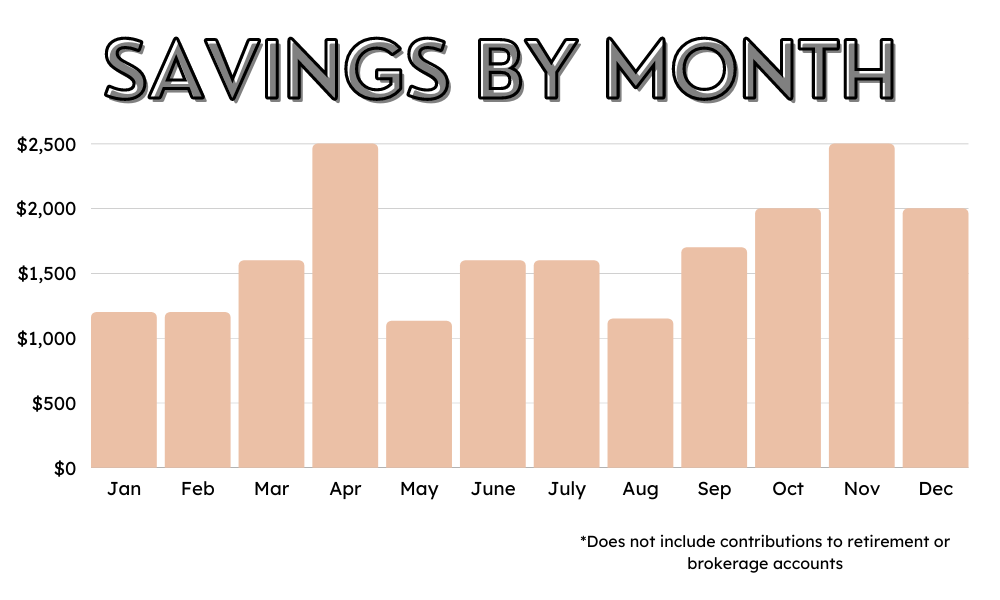

Savings

April and November were high savings months for us due to cash surpluses we had in both months. April was due to the stimulus payments – we qualified for the full $2,400 as a married couple and put half of it into our savings right away. November ended up being my largest income month ever (over $12k net) as my last paycheck from my previous employer included my PTO payout and annual bonus. As I mentioned above, I stopped contributing to my Roth IRA for a few months to beef up our savings. Thanks to my surplus in November, I was able to throw extra cash into our savings and also fully fund my IRA contributions for the year.

Overall, we were definitely aggressive with our cash savings this year. I can’t stress this enough – HAVE AN EMERGENCY FUND PEOPLE. My husband has been out of a job for nearly 9 months now and it wasn’t good fortune or a trust fund that allowed us to endure this hardship; it was disciplined financial planning.

Debt

Ah, my long-time frenemy: Debt. I haven’t rid myself of her just yet! This is always my favorite update for you guys ’cause I know so many of you can relate. A few days ago I shared on my Instagram story that I reached a milestone with my Roth IRA crossing the $50k mark. And while this isn’t an overly impressive benchmark by some people’s standards, I want to say that I have been solely responsible for paying for my college education. My parents did not have the means to put me through school, so I did it myself. If you combine my undergrad and grad school loans – I will have paid about $60k in tuition and fees BY MYSELF in 5 years. Do you know how much money I would have in my retirement accounts right now if I could have invested that $60k instead of paying it toward loans? A LOT. No, I don’t regret bearing the financial burden of putting myself through school – but I say all of this to say that it’s not just about numbers for me. So before you provide your backhanded compliments to me or anyone else choosing to be vulnerable and share their journeys: check your privilege and your attitude. OK back to our scheduled program.

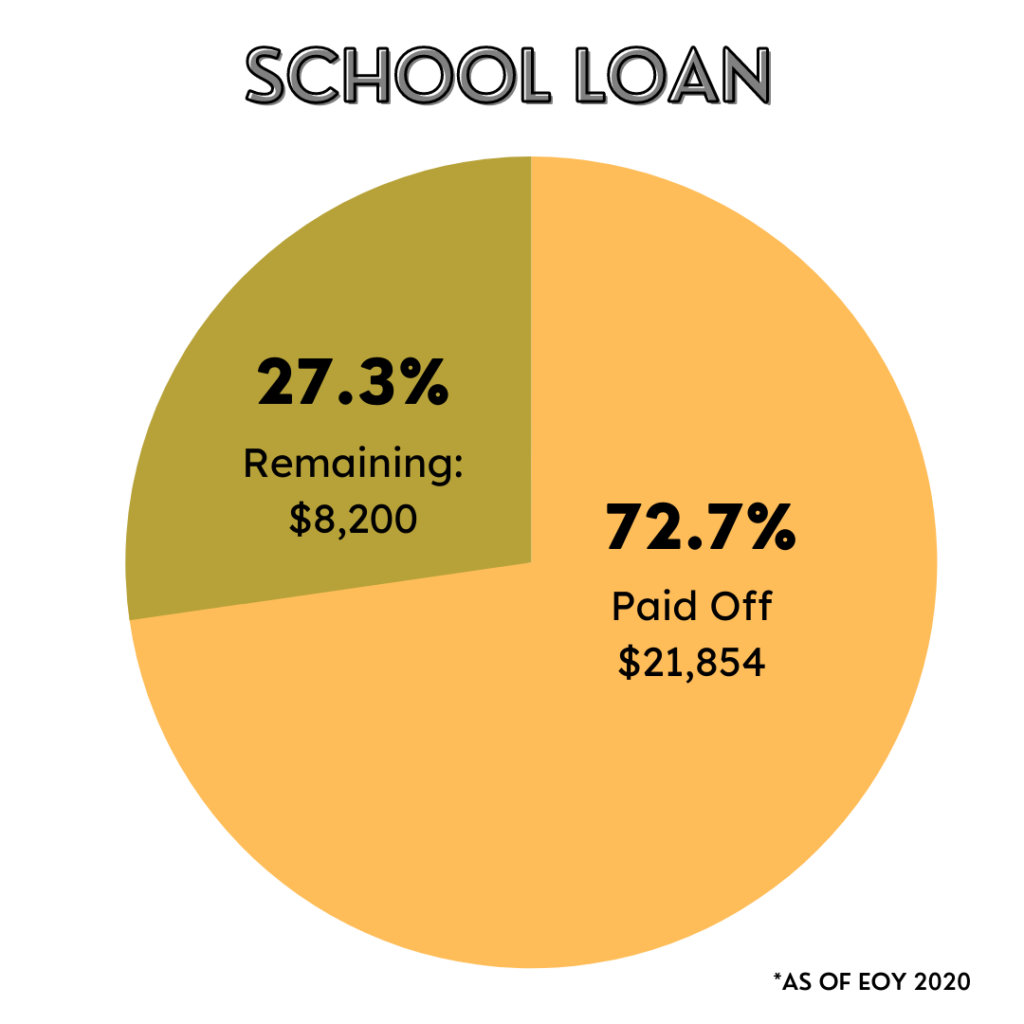

School Loan

As part of the CARES Act, the interest rates on all federal loans went to 0% in March. This is currently set to expire in December so I went HAM on paying down my school loans this year to take advantage of my payments going 100% toward the principal. Of my original $21k balance, I only have ~$8k left. IM IN THE FOUR DIGITS PEOPLE! Thanks to my cash surplus in November, I was able to put a large lumpsum toward my school loans. I’ll be increasing my payments in 2021 from $800 a month to $1400 to have my loan fully paid off by June(ish) 2021.

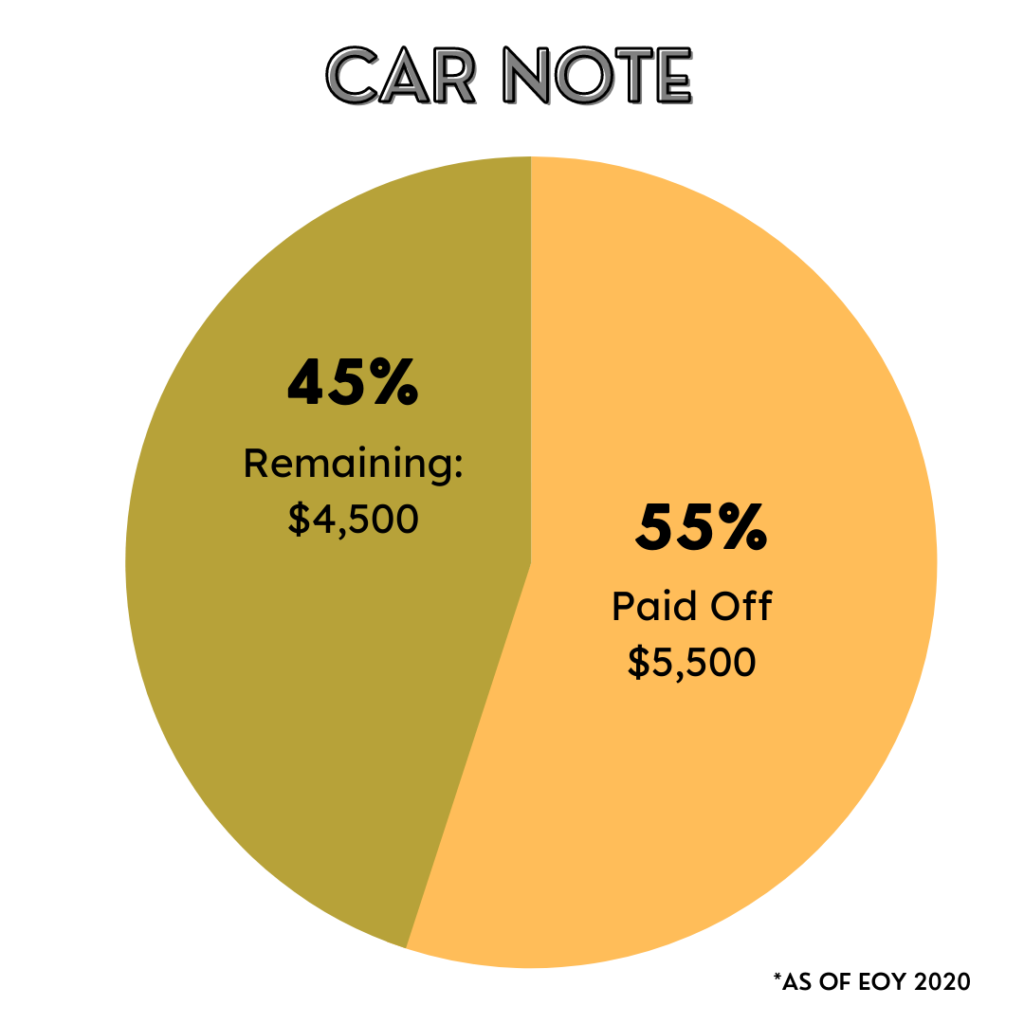

Car Note

I bought my car just last year and have a little less than half of the remaining loan left to pay. I plan to take $4,500 out of our savings account to pay off the remaining amount at the end of the year. Then, between Tommy and I – we’ll be free of car notes! Both of our cars are in excellent condition and should last for years to come, but Tommy has started to make noise about upgrading to a new truck. Why that little….

Looking ahead to 2021

There’s so much to look forward to in 2021. For starters, I’ll finally be debt-free (outside of our mortgage – which we have no intention of paying down early for several reasons)! It seems inconceivable that I’ve accomplished as much as I have and am so close to my debt-free finish line. Still, I have several plans for the upcoming year which include:

- Increasing my 401(k) contributions by 2%

- Maxing out my Roth IRA at $6,000

- Maxing HSA contributions of $3,550

- Increase monthly contributions to brokerage account by $200

- Increase monthly cash savings by $200

Love love love reading your blog! Thank you for sharing such valuable information! So grateful for you!

Thank you so much Linh!!! Your support and encouragement always means so much to me <3

Excellent point regarding having an emergency fund. I had my truck’s engine go out last year and I had to sell some assets to cover it. I would not have needed to have done that if I had an emergency fund.

Sooo….good point.